Quick note before we get started: I’m publishing this post publicly to ALL subscribers, free & paid because of how large this overhaul is. Going forward we’ll be back to paid subs getting signals with a 48 hour lead-time.

The Macro Regime Engine just went through its most significant overhaul since I rebuilt it fully in Python.

I’m going to be straight with you as always. I don’t sugarcoat, exaggerate or bend the truth. The numbers don’t lie and if there’s one thing I’m good at; it’s publishing the truth.

The TradingView MRE engine.. the one myself & all of you have been following.. went risk-off on March 10th. It just flipped back to risk-on today as of market close.

If you were following that signal, you sat in cash through the recent drawdown, subsequent rally back to highs and you’re now getting the green light to re-enter.

But behind the scenes, I’ve been building something better.

The Python version of the engine (V04).. which I’ve been testing, refining and tuning over the last several months, also went risk-off around the same time. As of tonight, it’s still sitting in Deflation, risk-off, 0% position. If I was running V04 unchanged, we’d still be in cash.

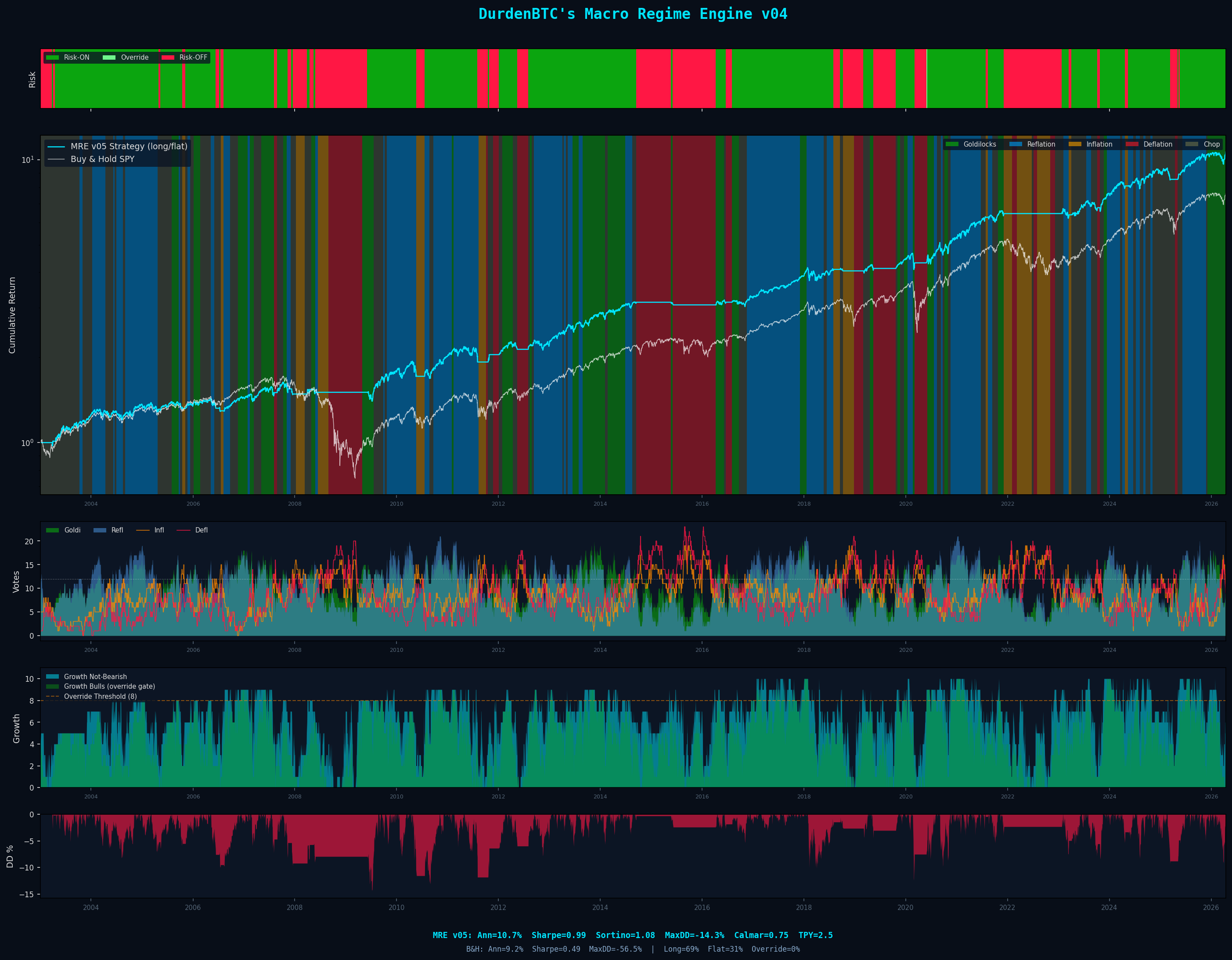

But I’m not running V04 anymore. I’m running V05. And V05 never went risk-off. It held through the entire selloff and is currently sitting in Goldilocks, risk-on, 100% position.

Before you think I’ve lost my mind.. let me show you the numbers.

A few things jump out:

TradingView has a great max drawdown (-17.3%) but the lowest annual return of the three (8.83%). It’s also the most conservative, only long 60% of the time. It misses a lot of upside by being in cash too often.

V04 flips the opposite way.. higher return (10.14%) by staying long more often (75.4%), but the max drawdown balloons to -21.1%. That’s the tradeoff I wasn’t comfortable with.

V05 threads the needle. Highest return (10.69%), best Sharpe (0.991.. nearly crossing the 1.0 threshold), lowest max drawdown (-14.3%), and a Calmar of 0.745. It does this at 2.5 trades per year.. barely more than V04’s 2.3 and less than TradingView’s 2.9.

What Changed in V05

Two independent improvements, both validated out-of-sample:

1. VAMS Parameter Tuning. I ran 7,500+ full portfolio backtests sweeping the parameters on all 22 TradingView assets. Found three where the settings were measurably suboptimal: T10YIE (10-Year Breakeven Inflation), [Redacted], and [Commodities]. The original parameters were ported from TradingView’s Pine Script but they were never optimized for the Python engine’s exact numerics.

Then I validated the changes out-of-sample. Split 23 years of data in half. Trained on 2003-2014. Tested on 2015-2026. The improvements didn’t just hold up.. they got stronger in the out-of-sample period. Sharpe improvement retention: 275%. Rolling 5-year window win rate: 9 out of 10.

2. Arsenal SPY Veto. The standalone Arsenal SPY indicator, which uses a completely independent signal based on pure OHLC math, no macro inputs now acts as an emergency brake.

If Arsenal goes fully bearish while the MRE is long, we exit to cash. Arsenal can’t trigger entries. Only the MRE can put us in. But Arsenal’s faster volatility detection catches acute crisis events before the macro voting matrix can react.

The combined effect: Sharpe goes from 0.815 to 0.991. Max drawdown drops from -21.1% to -14.3%. And we only add 0.2 trades per year.

What This Means Right Now

All three engines at the time of this writing:

TradingView: Risk-on (flipped today after market close)

V04 (Python): Risk-off (still in Deflation.. this would have been wrong)

V05 (Tuned+Veto): Risk-on (never left.. still in Goldilocks regime)

V05 is the engine going forward. The dashboard, the signals, the flash alerts, everything updates to V05 starting now.

This engine is not reliant on TradingView. It runs entirely in Python on my own infrastructure. I can test it, validate it, forward-test it, and export every signal day by day.

That’s the level of confidence I need before I put my money.. and your trust.. behind it.

Deployment Plan: Getting Back In

Given that we’re near all-time highs and I’m switching engines, I’m going to DCA into the equity position rather than lump-sum.

I know what the research says. Vanguard’s study found LSI outperforms DCA about two-thirds of the time, with an average outperformance of 2.3 percentage points.

Statistically, I should just deploy and move on. But there are a few important nuances that the headlines miss:

From a risk-adjusted perspective, only a 3-month DCA window is comparable to LSI. Beyond that, the opportunity cost of uninvested capital starts to dominate. A US Air Force Academy study found that DCA schedules of four months or longer produce statistically lower Sharpe ratios than LSI. So if you’re going to DCA, keep it tight.

The behavioral edge is real. Fidelity found that lump-sum investors are 37% more likely to panic sell during drawdowns. The math for LSI is better on paper. The outcomes for DCA are better in practice.. because people actually stick with it.

Augmented DCA outperforms standard DCA. Academic research on “Augmented DCA” (adjusting deployment size based on current conditions) shows improved risk-adjusted returns compared to both fixed-schedule DCA and LSI. Deploying larger amounts during favorable conditions and accelerating purchases during dips is a mild version of this approach.

My plan:

25% per week over 4 weeks starting tomorrow at market open.

Full position target within the next ~30 days.

If we get a >1% down day during any week, I’ll accelerate that week’s tranche early.

The research on “buying the dip” as a standalone strategy is actually poor, even with perfect omniscient timing of every market bottom, DCA beats buy-the-dip over 70% of the time..

But using dips to accelerate an existing deployment schedule is different. You’re not waiting for dips. You’re deploying on schedule and pulling forward a purchase you were going to make anyway.

For subscribers.. three options:

LSI (most aggressive): The system says risk-on. Deploy in full. That is what the backtest assumes. You are not wrong to do so. If you can handle watching a 5-10% drawdown the week after going all-in without touching anything, this is the highest expected return approach.

4-Week DCA (what I’m doing): 25% per week, accelerated on >1% down days. Full position within the month. Research-backed sweet spot that balances opportunity cost against behavioral risk.

Personal pace DCA: Scale in at whatever cadence lets you sleep at night. 33% over 3 weeks. 50/50 over 2 weeks. The system is risk-on. How you get to 100% is up to you. Just get there.

The one thing I’d advise against: stretching DCA beyond 4-5 weeks. At that point the opportunity cost of uninvested capital starts working against you and you’re effectively making a market timing bet disguised as risk management.

Why V05 and Why Now

I know changing engines raises questions. Here’s my answer: all alpha decays. Markets evolve. The parameters that were optimal in 2020, 2015 and 2005 aren’t necessarily optimal in 2026.

The key advantage of rebuilding this entire system in Python independent of TradingView was always about reaching this moment.

The ability to run exhaustive parameter sweeps, validate out-of-sample, test overlays, and iterate with confidence. I couldn’t do any of that on TradingView. Now I can.

I’ll be posting all the forward tests, the full backtest numbers and more in the next few weeks here on Substack. Along with that, all of the data and the live signals (updated nightly ~9:30PM EST) will be available on DurdenBTC.com members only dashboard by the end of April.

For those of you who’ve been with me since the beginning.. thank you.

We’ve gone from a Pine Script indicator to a full standalone engine with 25+ macro voters, 4 Arsenal indicators (more coming soon), out-of-sample validation, and now a Sharpe ratio that gets us to 1.0.

The edge keeps compounding. And we’re just getting started.

The engine says risk-on. Let’s go to work.

— Durden out.

✊🧼

Disclaimer: This content is for educational and informational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any asset. Trading equities and futures involves substantial risk of loss, including the potential for loss exceeding your initial investment.

Past performance, whether backtested or live, does not guarantee future results. Backtested performance has inherent limitations: it is designed with the benefit of hindsight, does not reflect actual trading, and does not account for all factors that may affect real-world execution.

The author is not a licensed financial advisor. Always do your own research and consult a qualified financial professional before making investment decisions. You are solely responsible for your own trading decisions.

Want the live dashboards behind these insights?

Subscribe on Substack Free subscribers get research updates. Paid subscribers get live macro tools + signal alerts.