Volatility Is Not Free

There is a persistent myth in investing especially in Bitcoin and crypto, that volatility is simply the "price of admission" to an exponential asset. That you must stomach the drawdowns to earn the returns. That any attempt to manage risk is market-timing, and market-timing doesn't work.

This is mathematically wrong. Volatility has a direct, quantifiable cost. It's called volatility drag, and it silently destroys wealth by forcing you to compound from lower values after every drawdown.

The core arithmetic is simple: losses are asymmetric. A −50% drawdown requires a +100% gain just to break even. A −75% drawdown, which Bitcoin has experienced three times.. requires a +300% recovery. Every dollar that survives a drawdown is compounding from lower nominal values, not from a peak.

| Drawdown | Recovery Required | Asymmetry Ratio |

|---|---|---|

| −10% | +11.1% | 1.1× |

| −20% | +25.0% | 1.3× |

| −30% | +42.9% | 1.4× |

| −50% | +100.0% | 2.0× |

| −75% | +300.0% | 4.0× |

| −85% | +566.7% | 6.7× |

The relationship is non-linear. Below −50%, the recovery math becomes brutal. This isn't a matter of opinion or risk tolerance, it's compounding arithmetic.

Two portfolios can have the same average arithmetic return and wildly different terminal values. A portfolio that returns +50%, −40%, +50%, −40% has an average return of +5%/year.. but the geometric return (what you actually earn) is −5.1%/year. The volatility consumes the entire return and then some. This is volatility drag.

Compound at a Higher Base

The thesis is not "time the market." The thesis is not "sell the top and buy the bottom." The thesis is structurally narrower and mathematically grounded:

If you can remove the fat left tail from the return distribution[1], even at the cost of surrendering the tip-top of the right tail, the sequence of returns means you will compound at higher portfolio values, and higher portfolio values at every stage of compounding equals more terminal wealth.

This is the key insight 95% of people miss. They see a risk-managed strategy underperform during a vertical move and conclude it "doesn't work." But they're measuring the wrong thing. They're measuring return per cycle when they should be measuring terminal portfolio value across all cycles.

An Illustrative Example

Steady gains, no drawdowns.

Compounding on a growing base.

Higher peaks, deeper valleys.

Compounding from a crater.

Both portfolios are invested in the same asset class. The unmanaged portfolio actually had a higher peak ($250K vs. $210K). But the −50% drawdown forced it to compound from $125K instead of $210K. By Year 3, the risk-managed portfolio is ahead by $149K.. a 79% advantage.. not because it captured more upside, but because it avoided compounding from a devastated base.

"The sequence of returns matters more than the average of returns."

This is the mathematical reality that the "just buy & hold" crowd ignores. They assume path-independence.. that only the destination matters. But compounding is path-dependent.[2] The order in which returns arrive determines the terminal value. A −75% early in the sequence is catastrophically more damaging than the same −75% late, because it destroys the base upon which all future gains compound.

The "Secular Uptrend" Fallacy

The most common objection: "Bitcoin is in a secular exponential uptrend. Why would you try to manage around drawdowns when the trend will eventually bail you out?"

Let's examine this carefully.

What Does "Secular" Actually Mean?

A secular trend is typically defined as a long-duration market movement lasting 10 to 40 years, driven by structural forces (demographics, technology adoption, monetary regimes). Bitcoin has been in a secular uptrend for approximately 15 years (at time of this writing). That places us somewhere in the middle of the typical secular window.. not at the beginning, where you can assume infinite runway, and not at the end.

Saying "we're in a secular uptrend" is true. But it's not an argument against drawdown management. It's a description of the environment in which you should be managing drawdowns. Secular uptrends don't eliminate volatility, they contain volatility. The question is: do you let that volatility compound against you, or do you manage it?

The Drawdowns Inside Bitcoin's "Secular Uptrend"

| Year | Drawdown | Recovery Required | Time to New ATH |

|---|---|---|---|

| 2011 | −93% | +1,329% | ~2 years |

| 2014–15 | −85% | +567% | ~3 years |

| 2018 | −84% | +525% | ~3 years |

| 2022 | −77% | +335% | ~2 years |

Every one of these occurred inside the secular uptrend. The trend didn't prevent them. And each one forced holders to compound from a devastated base for 2–3 years just to get back to where they started.

A dollar that survived the 2022 drawdown needed to 4.35× itself just to break even. A dollar in a risk-managed portfolio that avoided the drawdown was compounding on its full value the entire time. After the recovery, the managed dollar is still ahead.. permanently.. because it never fell behind.

Position Sizing Advice Debunked

The typical advice: "If you can't handle the volatility, reduce your position size." This sounds sensible, but think about what it actually implies. If you size down your position enough to emotionally tolerate a −75% drawdown, you've also sized down your exposure to the upside by the exact same proportion. You've traded volatility drag for opportunity cost. The wealth destruction is just happening through a different mechanism.

The alternative: keep the position meaningful, and manage the tail risk directly. This lets you participate in the secular trend with real capital while shaving off the catastrophic left-tail events that destroy compounding.

Two Systems, One Philosophy

The philosophy is asset-agnostic. The implementation is asset-specific. Two purpose-built systems apply the "Survival Is Alpha" thesis across the two primary asset exposures:

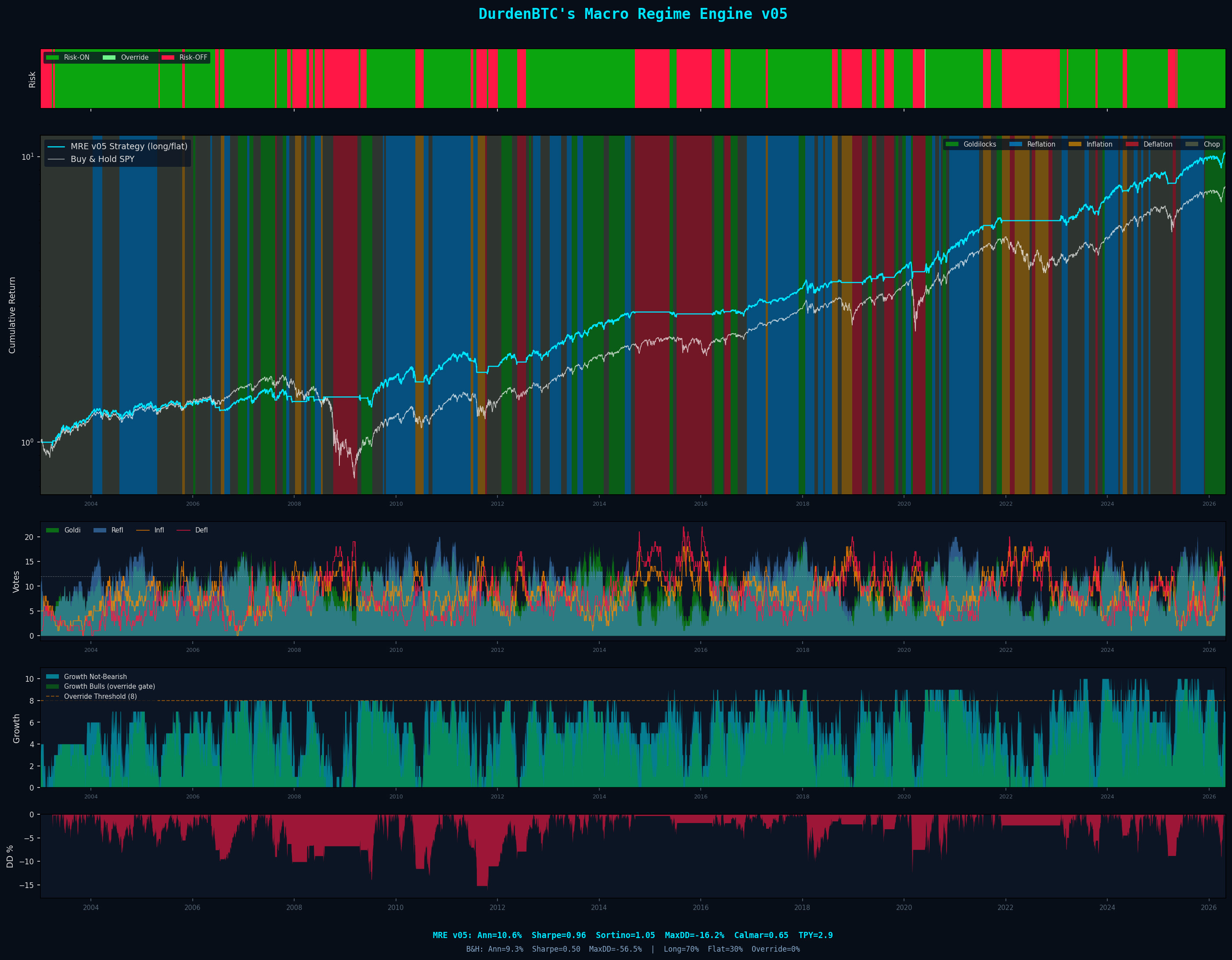

For Equities (S&P 500): MRE v06 — The Macro Regime Engine

A multi-asset voting system that polls 26 global assets across equities, breakevens, duration, FX, the curve, and credit. Each asset calculates a volatility-adjusted trend signal and casts votes into four macro regime buckets: Goldilocks, Reflation, Inflation, and Deflation.

The system makes a binary decision: is the global macroeconomic environment friendly to equities? If yes, hold SPY at 100%. If no, hold cash. No discretion. No "nibbling." No hope trades. Symmetric hysteresis prevents whipsaw; an Arsenal SPY veto layer catches the cases where macro looks fine but equities are imploding on their own.

MRE v06: +925.8% · CAGR: 10.52% · Sharpe: 0.96 · Max DD: −16.22%

Buy & Hold SPY: +679.4% · CAGR: 9.22% · Max DD: −56.47%

5,867 trading days. 26 voters. Seven independent forward tests, zero failures. The strategy outperformed buy-and-hold while spending 30% of trading days in cash.. precisely the days that produced the buy-and-hold drawdowns.

How It Dodged Every Major Crash

The engine didn't predict these crashes. It measured that the macroeconomic environment had turned hostile: credit spreads widening, volatility spiking, growth currencies collapsing, safety assets rallying.. and stepped aside before the waterfall phase. The edge isn't prediction. It's measurement.

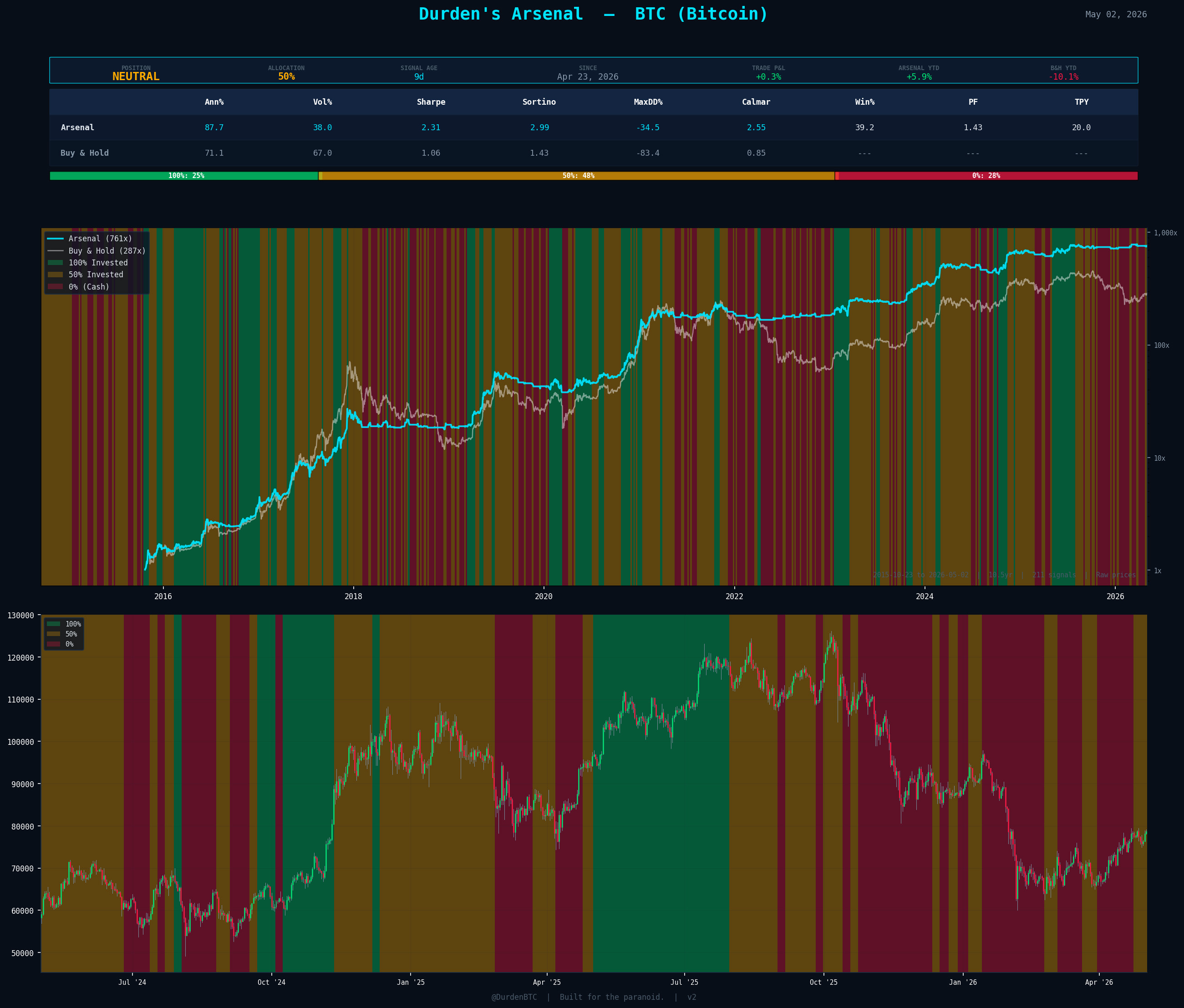

For Bitcoin: Arsenal BTC — The Bitcoin Trend System

A three-state trend system built on VAMS.. a composite of an SMA-crossover trend filter and a three-layer volatility regime filter (calm-bull, calm-bear, crisis). Output is a single vote: +2 BULLISH (100% long), 0 NEUTRAL (50% long), or −2 BEARISH (0%, cash). No leverage, no discretion.

Bitcoin requires a different system than equities because its return distribution is fundamentally different: fatter tails, higher kurtosis, and vol spikes that reverse in a week. The vol-regime layer is a kill-switch that fires before the trend signal has a chance to give back gains.. which is exactly when a naive trend system gives back a year of upside in a flash event.

Arsenal BTC: +78,930% · CAGR: 87.75% · Sharpe: 2.32 · Max DD: −34.46%

Buy & Hold BTC: +32,563% · CAGR: 72.73% · Max DD: −83.40%

Captured most of Bitcoin’s upside while cutting drawdown by more than half. Three of four forward tests pass; the OOS walk-forward verdict is honestly disclosed as WEAK on the forward-testing page.

One philosophy across both engines. MRE v06 reads breadth across 26 macro voters and outputs a binary risk-on/off SPY signal. Arsenal BTC reads price-and-vol on a single asset and outputs a three-state position (100% / 50% / 0%). Different problems, different tools, identical disciplines: daily-close execution, full backtest disclosure, and forward-test honesty.. including the WEAK results when they happen. The 8th Rule (our older, more aggressive Bitcoin system) is still available to subscribers who prefer it, but Arsenal BTC is the flagship.

The Operating Commandments

Cash Is an Asset Class

In periods of chop, regime conflict, or hostile macro, cash (via $SGOV or $USFR) is the active position. It preserves purchasing power and critically preserves the compounding base from which the next move compounds.

No Hope Trades

If the system says Neutral or Bearish, the position is zero. No "nibbling," no "DCA into weakness," no "it looks like a bottom." Buy strength or hold cash. Drawdowns are not buying opportunities: they are the enemy of compounding.

Respect the Regime

Never fight the macro tide. If the regime says Inflation or Deflation, do not hold a Goldilocks portfolio because you "like" the stocks. The engine's 20+ asset consensus overrides individual conviction.

Accept the Right-Tail Cost

Any risk management framework will clip some upside during vertical rallies. This is the trade. You surrender the top 5% of the right tail to remove the bottom 20% of the left tail. The compounding math makes this trade overwhelmingly positive over time.

Sequence Over Average

Never evaluate performance by average return. Evaluate by terminal wealth. Two portfolios with identical average returns can diverge by hundreds of percent based on the order of those returns. The sequence is everything.

Why This Wins

The entire thesis reduces to one sentence:

"You don't need to capture more upside per cycle.

You need to avoid the catastrophic losses that destroy compounding."

MRE v06’s +925.8% vs. buy-and-hold SPY’s +679.4% over 23 years is almost entirely explained by dodging the major drawdowns.. 2008, 2020, 2022, 2025. The system didn’t capture more upside than the market per bull cycle. It just never compounded from a crater.

A −16.22% max drawdown vs. buy-and-hold’s −56.47% means the system was compounding from near its peak value after every single macro shock. Every dollar in the strategy had a dramatically higher starting base entering the next bull cycle. Over 23 years that differential.. that permanently higher base.. compounds into a +246 percentage-point outperformance gap, with a Sharpe nearly twice that of buy-and-hold.

The Bitcoin side tells the same story with bigger numbers. Arsenal BTC’s −34.46% max drawdown vs. buy-and-hold BTC’s −83.40% means the system enters every new bull cycle compounding from less than half the buy-and-hold drawdown. That asymmetry is the entire reason its 78,930% total return blows past buy-and-hold’s 32,563%.. despite spending material time in cash.

This isn't market timing. This isn't mean reversion. This is drawdown management as a compounding strategy. Truncate the left tail, accept a modest right-tail cost, and let the math do the rest.

Survival isn't a consolation prize. It's the highest-alpha strategy in existence because every dollar that survives compounds forever, and every dollar that drowns in a drawdown compounds from zero.

Footnotes

- Moreira, A. & Muir, T. (2017). Volatility-Managed Portfolios. Journal of Finance, 72(4), 1611–1644. The empirical anchor for vol-targeted sizing as a Sharpe-improving strategy. Demonstrates across equities, bonds, currencies, and commodities that scaling exposure inversely to recent realized volatility — i.e., truncating the left tail at its source — lifts risk-adjusted returns. The reason the thesis can claim "remove the fat left tail" as an empirically grounded operation, not a hand-wave. SSRN →

- Kelly, J. L. (1956). A New Interpretation of Information Rate. Bell System Technical Journal, 35(4), 917–926. The original derivation of the optimal growth-rate criterion under uncertainty. Establishes that the geometric (compound) growth rate of capital is path-dependent and that position sizing — not selection — sets the long-run rate of return. The mathematical anchor for why "compounding is path-dependent" isn't a metaphor; it's the only relevant arithmetic. Princeton PDF →

See the full reading list — DurdenBTC Academic Foundations →