Most of you know me for the Macro Regime Engine, The 8th Rule, and the weekly signal updates. But there’s a small sleeve of my portfolio that I rarely talk about.. and it’s one of the most consistently profitable things I run.

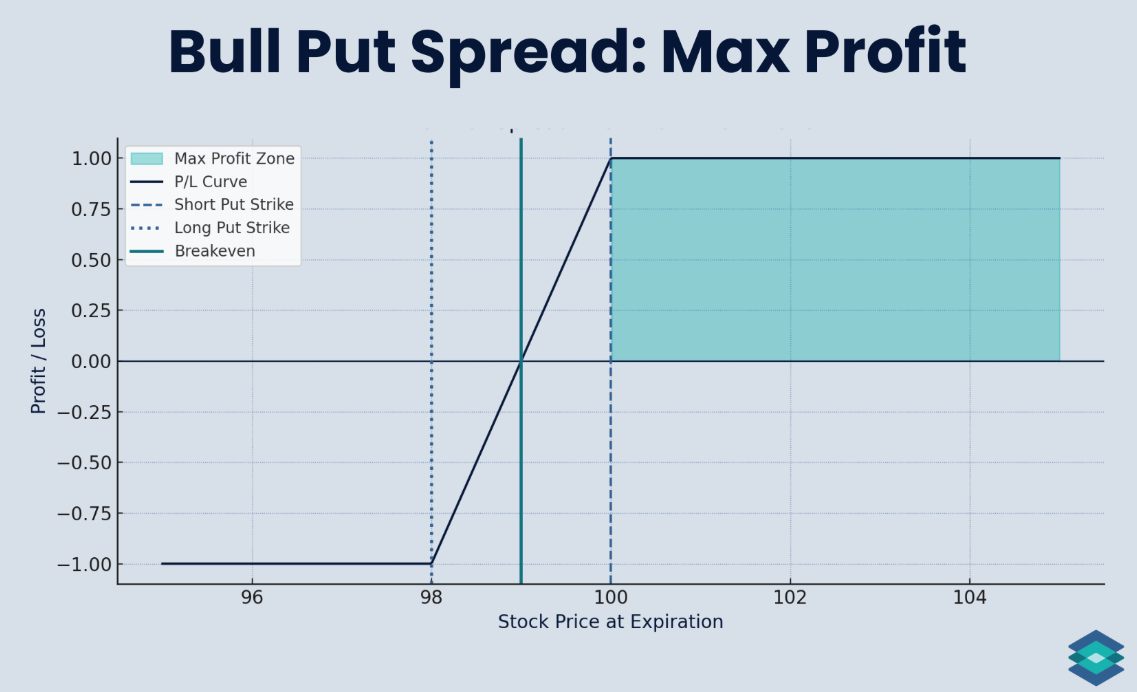

It’s a bull put spread on . 2-4% of total portfolio. Nothing sexy. Nothing leveraged to the gills. Just a simple, systematic options income strategy that only activates when my Macro Regime Engine says it’s safe to play offense.

The Setup

Here are the rules. No ambiguity. No vibes.

Entry: Choose the nearest expiration to 45 DTE (days to expiration).

Strike Selection: Sell a 15-25 delta bull put spread on $SPY. When the regime is in early Goldilocks specifically, I push it up to 25-35 delta because the macro tailwinds are strongest.

Exit: Close the position at 21 DTE regardless of P&L. Win, lose, or draw.. you close.

Recycle: Immediately re-open the same structure at 45 DTE. Rinse and repeat.

Kill Switch: The moment my Macro Regime Engine flips to risk-off (Inflation or Deflation), I close the spread and walk away. No exceptions.

That’s it. No profit targets. No stop losses. You manage exclusively on time. Enter at 45, exit at 21, re-enter at 45. A mechanical income loop that runs as long as the regime says “go.”

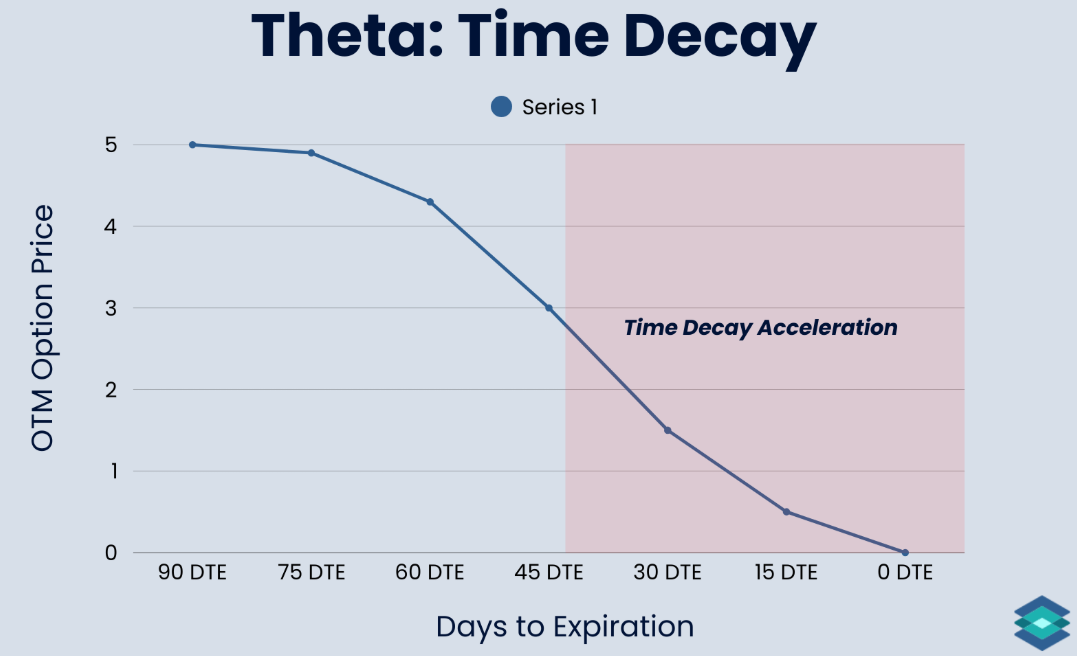

Why 45 DTE? The Research Is Clear.

I didn’t pull these numbers from a hat. This framework is heavily influenced by research from TastyTrade, Options with Davis, and Data Driven Options.. all of whom have done extensive backtesting on optimal trade duration for short premium strategies.

The core finding across all of them is the same: 45 DTE is the sweet spot for selling options.

There are two forces at play here.

Theta decay accelerates. Options lose value as time passes, and that decay starts meaningfully picking up around the 45-day mark. By entering at 45 DTE, you’re positioning yourself right at the inflection point where the clock starts working hardest in your favor. The short put decays faster than the long put.. that differential is your edge.

Implied volatility consistently overstates realized volatility1. This is the big one. A Cambridge Associates study found that implied volatility has overestimated historical (realized) volatility roughly 85-87% of the time on SPX options dating back to 1990.

Think about what that means for a second. The market is systematically overpricing the expected move in the S&P 500 almost nine out of ten times. That’s not a fluke.. that’s a structural risk premium baked into options pricing. And every time you sell a put spread, you’re harvesting that premium.

Read that paragraph again because that’s the foundation of the entire edge here..

TastyTrade’s quantitative research team confirmed this with their own multi-year studies: 45 DTE entries managed at 21 DTE produced the best risk-adjusted daily P&L across all trade durations tested.

Jacob Perlman, a mathematician at TastyLive, put it simply: 45-day options offer predictability and lower risk during the initial hold period, which supports early management around the 21-day mark to lock in gains and reduce exposure.

Option Alpha’s backtest of SPY put credit spreads over five years found a 93% win rate with no consecutive losses when using structured entry and exit criteria. Data Driven Options found that the 45 DTE window, when paired with teen-delta spreads, produces the fastest-decaying spread combination.. meaning you’re capturing the most theta per dollar of risk.

The math converges from every angle. 45 DTE gives you enough premium to make the trade worthwhile, enough time for theta to work, and enough distance from expiration to avoid the gamma risk that destroys shorter-dated trades.

Why 21 DTE Exit? Gamma Is the Enemy.

Here’s the thing most people get wrong about credit spreads: the risk isn’t that you lose.. it’s when you lose.

As expiration approaches, gamma accelerates. That means small moves in the underlying start producing outsized changes in your spread’s value. A stock that was sitting comfortably 5% above your short strike can suddenly be testing it after one bad session.. and at 7 DTE, that move hits different than it does at 35 DTE.

By exiting mechanically at 21 DTE, you’re stepping off the tracks before the train picks up speed. You capture the bulk of the theta decay (the easy money), and you hand back the final 21 days (the dangerous money) to someone else. Then you immediately re-enter at 45 DTE and start the cycle again.

This isn’t about maximizing each individual trade. It’s about maximizing the system over hundreds of trades.

Why Only During Risk-On?

This is the part that separates this from a generic “sell premium” strategy.

A bull put spread is inherently a bullish-to-neutral position. You profit when SPY goes up, stays flat, or even drops a little. But you get crushed when SPY drops hard and fast.. exactly what happens during Inflation and Deflation regimes.

My Macro Regime Engine exists to tell me when the environment is favorable for risk assets. When we’re in Goldilocks or Reflation, equities have a structural tailwind. Growth is accelerating, liquidity conditions are supportive, and the probability of a violent drawdown is significantly lower (not zero.. never zero.. but lower).

Running a bull put spread during these conditions is like selling umbrella insurance on a sunny day. The premium you collect is real, the probability of payout is low, and the macro wind is at your back.

The moment the Engine flips to risk-off? I kill the spread. Immediately. I don’t wait for the spread to “recover.” I don’t hope. I close it and move to cash on that sleeve. The same discipline that keeps me out of Bitcoin during bearish trends keeps me out of bull put spreads during hostile regimes.

This is the edge that most options sellers don’t have. They run credit spreads 365 days a year and then wonder why one bad month erases six months of gains. They’re selling umbrellas in a hurricane.

I only sell when the weather forecast says clear skies.

Sizing: Small and Intentional

I run this at 2-4% of total portfolio capital at risk. That’s it.

Why so small? Because this isn’t the core strategy.. it’s the supplement. The Macro Regime Engine on $SPYM is my primary equity edge. The 8th Rule is my Bitcoin edge. VATS on $ACWX and $GLD handle the international and commodity sleeves. The bull put spread is just additional return on capital during favorable conditions.

Think of it like this: the core portfolio is the engine. The bull put spread is a turbocharger that only activates on the straightaways. You don’t need it to win the race. But when conditions are right, it gives you a little extra.

I’ve scaled in and out based on conviction before. Five contracts (five because the max loss lines up with 3% of my total portfolio value) early in the regime when conviction is highest, then four, then three as the regime matures. If I close for +70% profit ahead of a major catalyst (like NVDA earnings), I’ll reopen with slightly reduced size. Gradual de-risking as the easy part of the regime gets consumed.

The Bottom Line

The bull put spread on $SPY is not the flashiest thing I do. There are no Baroque oil painting thumbnails for this one. No dramatic regime calls. Just a quiet, mechanical income loop that compounds small wins during favorable macro conditions.

The research supports it. IV overstates realized vol ~85% of the time. 45 DTE is the optimal entry window. 21 DTE management captures the best risk-adjusted returns. And layering a macro regime filter on top ensures you’re only exposed when the environment favors the trade.

Systems within systems. Edges stacked on edges. That’s the whole game.

If you want to see this in action, I use OptionStrat to visualize the P&L before entry. Clean tool, highly recommend it.

For further research, I highly recommend this series of articles: https://datadrivenoptions.com/strategies-for-option-trading/favorite-strategies/credit-put-spread/

⚔️ Stay Sharp

Follow the Macro War Room every Friday for the only macro analysis that treats markets like the battlefield they are.

💥 Stay sovereign. Don’t be exit liquidity.

— Durden out. ✊🧼

Want the live dashboards behind these insights?

Subscribe on Substack Free subscribers get research updates. Paid subscribers get live macro tools + signal alerts.