What It Is

A systematic macro regime detection engine that aggregates volatility-adjusted trend signals from 20+ global assets to identify the current macro cycle, then positions capital accordingly.

No predictions. No narratives. Just data-driven regime classification and systematic execution.

The Framework

Most investors look at markets through two lenses: mean reverting or trending. If only it were that simple. Markets move in macro regimes.

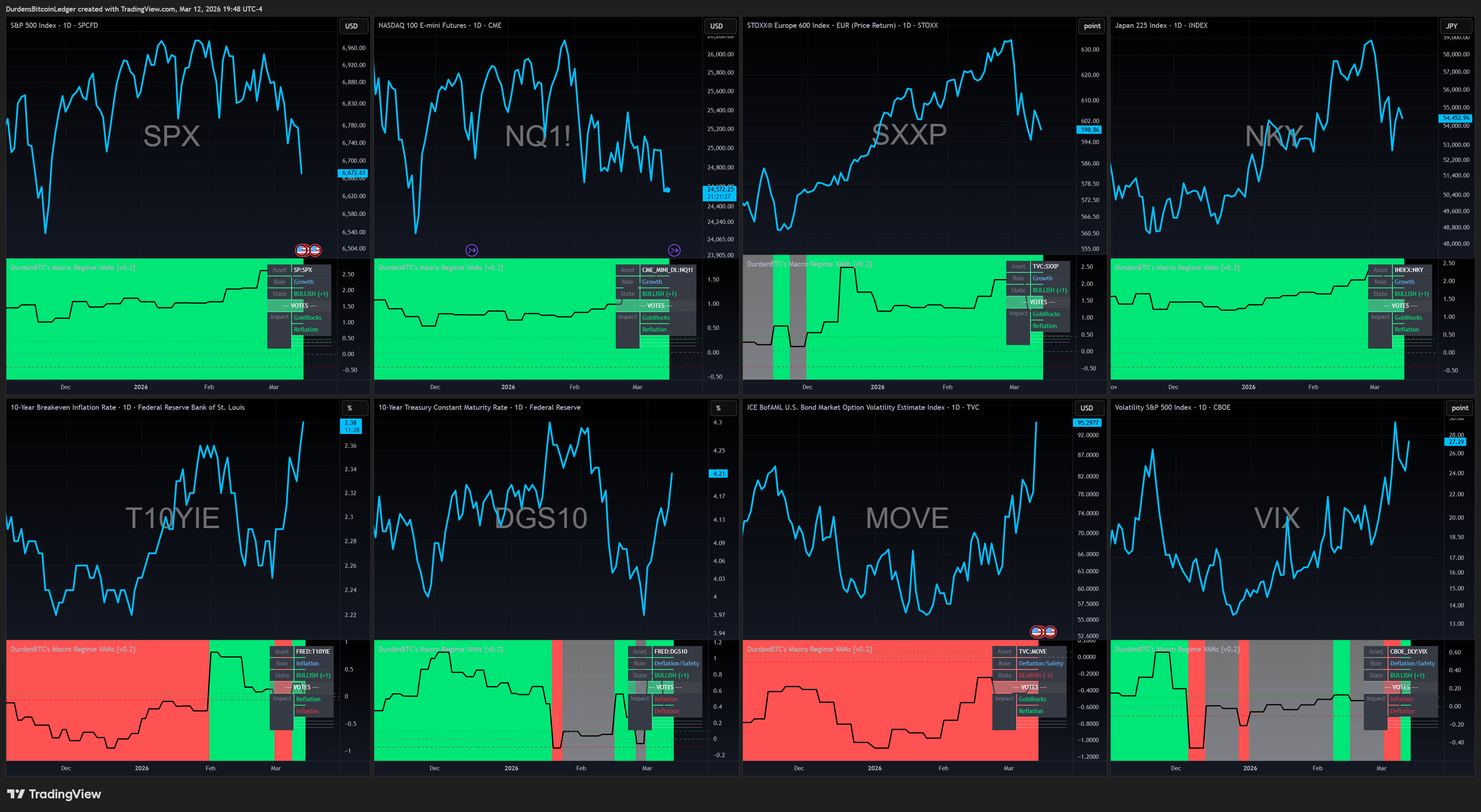

The MRE (Macro Regime Engine) classifies the current global macro environment into four distinct states:

🟢 Goldilocks (Risk-On)

Growth is strong. Inflation is contained. Credit is loose. Risk assets fly.

🔥 Reflation (Risk-On)

Growth is accelerating. Commodities are rising, inflation is trending higher. Central banks are still accommodative. Stocks and commodities both work.

🛑 Inflation (Risk-Off)

Inflation is rising. Central banks are tightening. Credit is stressed. Risk assets struggle. Volatility spikes.

❄️ Deflation (Risk-Off)

Growth is contracting. Fear is rising. Flight to safety. USD and bonds bid. Risk assets sold.

Each regime has different asset class winners and losers. The Engine detects which regime we’re in, then positions accordingly.

Simple. Systematic. Unemotional.

The Voting System

Here’s how the Engine determines the current regime:

I track 20+ global assets across multiple classes:

Equities: SPX, NDQ, RTY, [Redacted]

Crypto: BTC

Commodities: Oil, [Redacted]

FX: [Redacted]

Rates: 10Y yields, curve steepener, [Redacted]

Credit: High yield spreads

Volatility: VIX, [Redacted]

For each asset, I calculate a Volatility-Adjusted Trend Signal (VATS). Think of it as asking whether recent price movement is statistically meaningful relative to current noise.

Each asset with conviction then casts weighted votes into regime buckets based on what its behavior means macroeconomically. Growth assets rallying tells you something different than commodities rallying. Volatility spiking tells you something different than the dollar strengthening. The voting matrix maps each signal to the regimes it supports.

The regime with the most votes wins.

But there’s a filter: the new regime must hold the lead for 5 consecutive bars before the official signal flips. This prevents whipsaws while still catching major macro shifts early.

No FOMO. No panic. Just confirmation.

The “Bad News Is Good News” Override

This is one of the system’s most important features.

Sometimes the macro data says “deflation”.. yields are falling, the curve is inverting, breakevens are dropping, but equities are rallying anyway. This happens when markets are front-running the Fed: bad economic data means rate cuts are coming, and rate cuts are bullish for equities.

This was the dominant regime in late 2023 and early 2024. Textbook deflation. But equities rallied aggressively because the market was pricing in the pivot. A naive regime system would have been 100% cash during one of the best equity rallies in years.

The Engine has a built-in override for exactly this. When macro data says risk-off but growth assets disagree overwhelmingly, broad-based, not a dead-cat bounce.. the system sides with markets. Because markets price the next move while economic data reflects the current one.

When the market and the macro disagree, the market is usually right in the short-to-medium term.

The Trading Logic

The Engine doesn’t try to be clever.

Risk-On Regimes (Goldilocks or Reflation):

→ LONG ES futures (or SPX) (100% of equity determines contract quantity)

Risk-Off Regimes (Inflation or Deflation):

→ FLAT (exit to cash)

That’s it.

No hedging. No complex position management. Just binary risk-on or risk-off based on what the macro is telling us.

The Performance

I backtested this on ES futures from August 1999 to January 2026.

Here’s what happened:

Compare that to buy-and-hold SPX:

Total Return: 430%

CAGR: 6.51%

Max Drawdown: 50%+ (multiple times)

MRE delivered 16x the total return with 15x less drawdown.

For the complete backtest numbers & full analysis, please click here.

The Validation

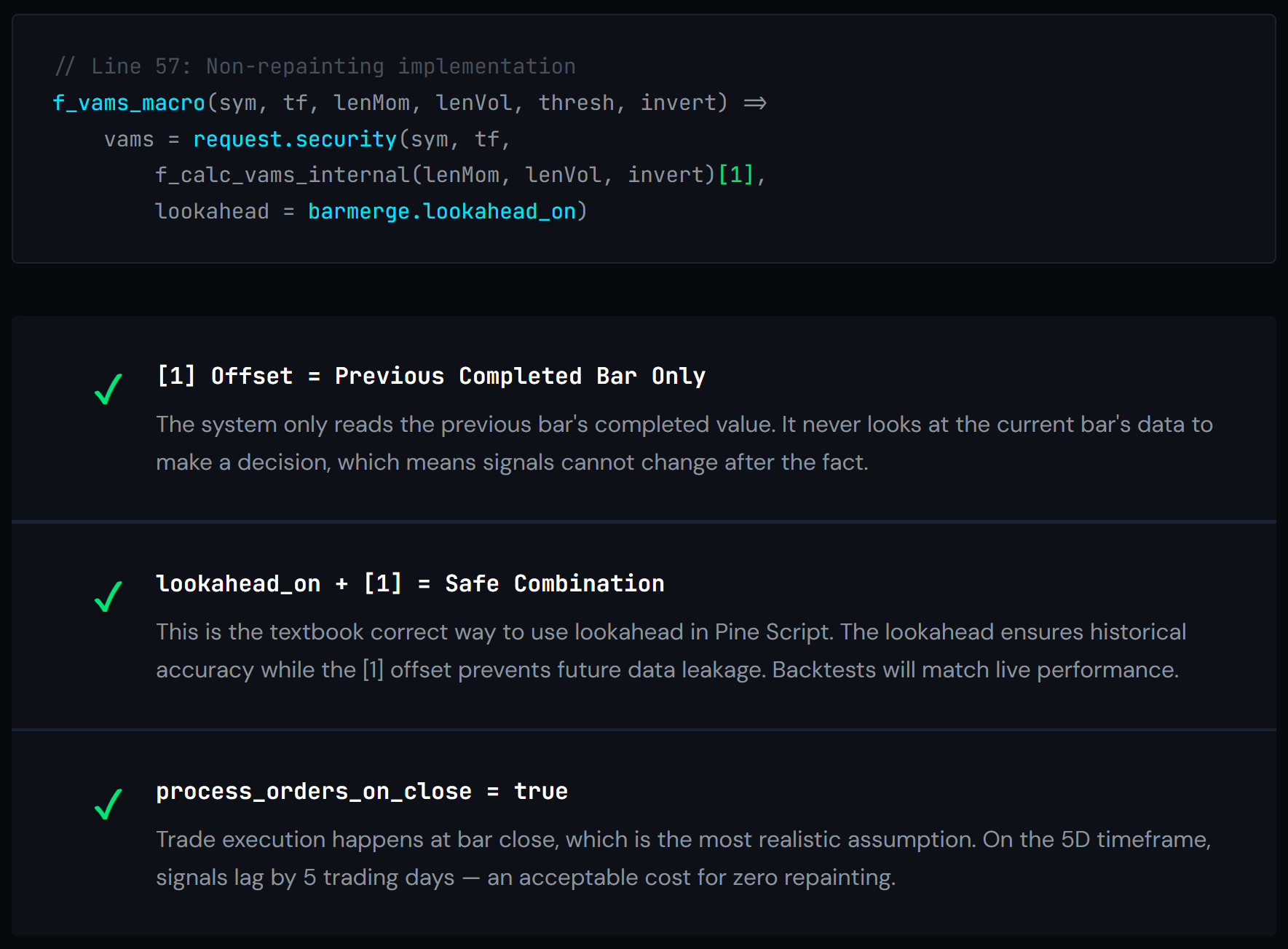

But here’s the thing: backtests lie. Often.

So I needed to verify this wasn’t some look-ahead bias, repainting, or TradingView glitch.

I built an independent Python script that:

Parsed the CSV of all 37 trades

Recalculated every P&L from entry to exit

Verified the equity curve step-by-step

Cross-checked against TradingView’s numbers

The result?

My calculation: $7,040,550

TradingView backtest: $7,040,528

Difference: $22 (0.0003%)

The numbers are real. The backtest is clean. The code is non-repainting.

I also code-reviewed the Pine Script implementation to confirm:

Verdict: Historical backtests will match live trading performance.

How It Survived 26 Years

This system went through:

Dot-com bubble (2000)

9/11 (2001)

Financial crisis (2008)

Flash crash (2010)

Euro crisis (2012)

I wrote an entire article about how the system side-stepped the entire COVID crash the week of. Feel free to check it out for a deep dive.

17.45% CAGR through all of it. With a ~5% max drawdown.

How?

It exits to cash during hostile regimes.

Look at the worst trades:

2012: -3.37% (Euro crisis, exited during Inflation regime)

2016: -1.28% (Brexit, regime uncertainty)

2019: -1.51% (Trade war chop)

Meanwhile, the best trades:

2020-2021: +48.48% (COVID recovery, Goldilocks regime)

2014: +34.93% (Post-GFC expansion, sustained Goldilocks)

2024: +13.82% (AI boom, Goldilocks)

The system doesn’t avoid all losses but it avoids the big ones.

You don’t make money by holding through crashes. You make money by not being there when they happen.

The Real Edge

It’s not the 17% CAGR.

It’s the 5.96% max drawdown while delivering those returns.

Most traders focus on upside. The Engine focuses on not giving it back.

The streaks:

Max consecutive wins: 8

Max consecutive losses: 2

When it’s right, it stays right. When it’s wrong, it gets out fast.

Profit Factor of 17.41 means every dollar risked returned $17.41 in profit.

That’s not luck. That’s systematic.. and quite frankly, asymmetric.. risk management.

The math that makes this system demolish buy-and-hold isn’t the upside capture. It’s the drawdown avoidance. A portfolio that drops 56% (GFC) needs a 127% gain to recover. A portfolio that drops 5.96% needs a 6.3% gain. The Engine spent 2008-2009 compounding from near its peak while buy-and-hold was rebuilding from a crater. That differential compounds for the next decade.

The Trading Reality

37 trades in 26 years = 1.4 trades per year.

Average hold time: 159 days (about 5 months).

This isn’t day trading. This isn’t even swing trading.

This is macro positioning.

You could run this system with a full-time job. You could run it while traveling. You could run it while sleeping.

Because the Engine doesn’t care about intraday noise. It cares about regime changes. And regime changes happen slowly.

You get an alert when the regime flips. You execute the trade. You go back to your life.

That’s it.

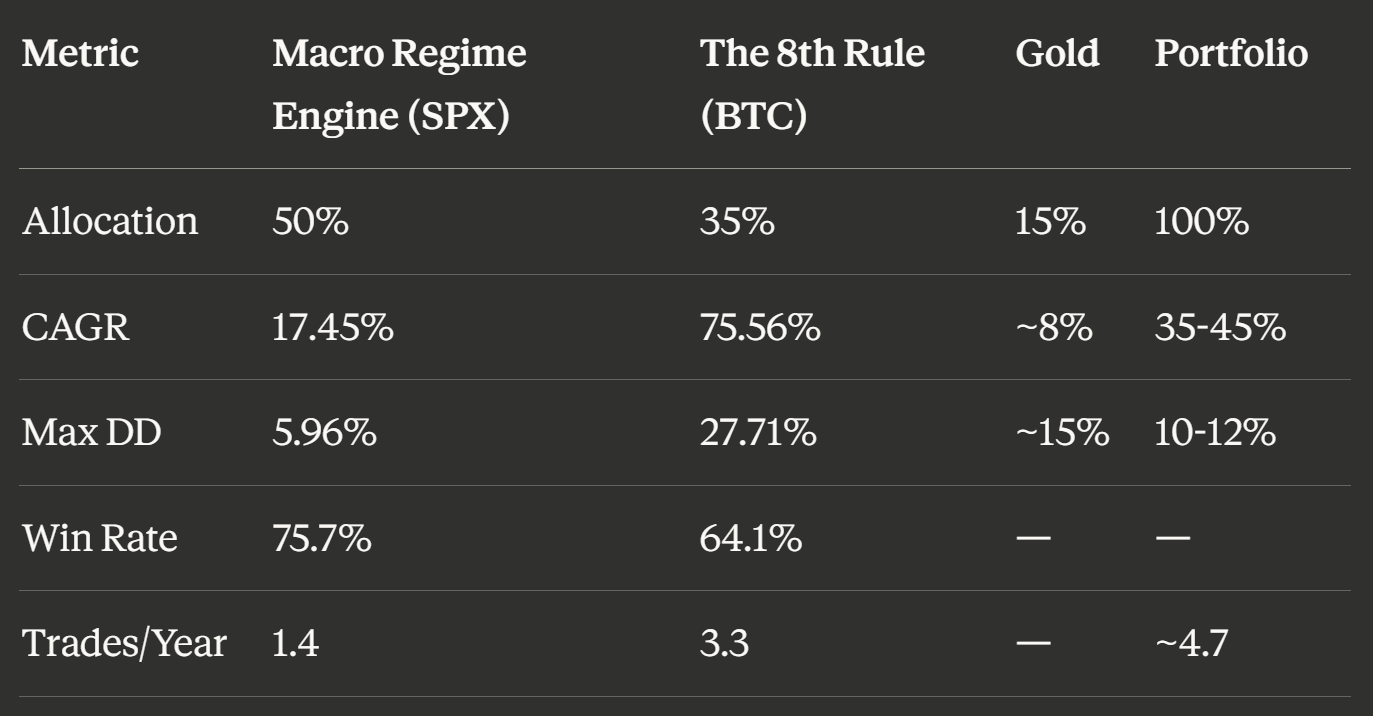

The Full Arsenal

The Macro Regime Engine handles equities. But that’s one system.

For Bitcoin, I built a separate engine: The 8th Rule.. a dual-speed Gaussian volatility trend system purpose-built for BTC’s unique volatility profile.

Where the MRE polls 22 global assets, The 8th Rule runs two independent signal engines at different speeds on BTC itself. A fast entry system catches trend flips within days. A slow confirmation system validates the move. Dynamic position sizing bridges the gap, you risk less during the uncertain window between the two, and scale to full conviction when both agree.

The combined portfolio:

Estimated portfolio Sharpe: ~1.5. Estimated Calmar: ~3.5.

The two systems have low correlation. When the MRE is flat (risk-off for equities), BTC might be in a completely different regime. When BTC corrects, the MRE is often riding a Goldilocks rally. Gold provides insurance when both are under stress.

Diversification that actually works.

Paid subscribers get signals from both systems.

What I’ve Shipped Recently

This isn’t a static system. I’m building in public, testing, iterating, publishing.

Delivered:

Portfolio rebalancing: replaced US-only equity allocation with a split between SPYM (MRE-managed) and ACWX (international, VATS-managed) alongside GLD and BTC/USFR. Full thesis published for paid subscribers.

Options overlay: bull put spread strategy (45 DTE, 25-35 delta, close at 21 DTE) as a 2-4% portfolio sleeve, active only during risk-on regimes. Another incremental edge on top of the core systems.

RealVision appearance: guest on Kris Bullock’s show breaking down the regime framework for a broader audience.

Signal #37: the first live risk-off signal, March 9, 2026. Subscribers had it in real-time.

In development:

Members only dashboard on DurdenBTC.com. Access global liquidity, stress overlays, macro weather & more.. live from your own personal dashboard.

Regime-specific asset rotation across inflation-protected, bond, and commodity instruments.

I publish the research, the reasoning, and the receipts.

Why It Works

The Engine works because it’s built on fundamental macro relationships:

Growth assets rise during expansions (SPX, BTC, [Redacted])

Commodities rise during reflationary periods (Oil, [Redacted])

Volatility spikes during stress (VIX, [Redacted])

Credit spreads widen during crises (HY spreads)

Currencies reflect macro flows (DXY, [Redacted])

These relationships are structural. They’re not going away.

As long as central banks exist, credit cycles exist, and risk-on/risk-off dynamics exist, the MRE will work.

It doesn’t predict the future. It detects the present.

And then it positions accordingly.

The Philosophy

Markets are driven by macro regimes, not micro narratives.

Trend followers chase price action and get chopped during regime transitions.

Stock pickers focus on company fundamentals and get blindsided by macro shifts.

Narrative traders follow headlines and get wrecked when the story changes.

Regime traders stay solvent.

Because they understand: the macro drives the micro. Every. Single. Time.

You don’t need to predict what Powell will say next month.

You don’t need to guess if we’re in a recession.

You don’t need to time every move perfectly.

You just need to know: What regime are we in right now?

And position accordingly.

Bottom Line

$100,000 → $7,040,528 isn’t luck.

It’s systematic macro regime detection.

It’s multi-asset consensus building.

It’s ruthless risk management.

It’s patient compounding.

Price leads news. Regimes drive returns. Risk management is the edge.

Most traders will never understand this. They’ll keep chasing narratives, timing tops and bottoms, and getting chopped.

But you’re here. You’re reading this. You’re thinking systematically.

Trade the regime. Not the headline.

Stay liquid, not wrecked.

📌 Want more macro signal?

Subscribe for:

Real-time regime updates

Multi-asset voting breakdowns

Backtested strategy insights

No noise. Just signal.

👉 Subscribe to Durden’s Macro War Room

Want the live dashboards behind these insights?

Subscribe on Substack Free subscribers get research updates. Paid subscribers get live macro tools + signal alerts.