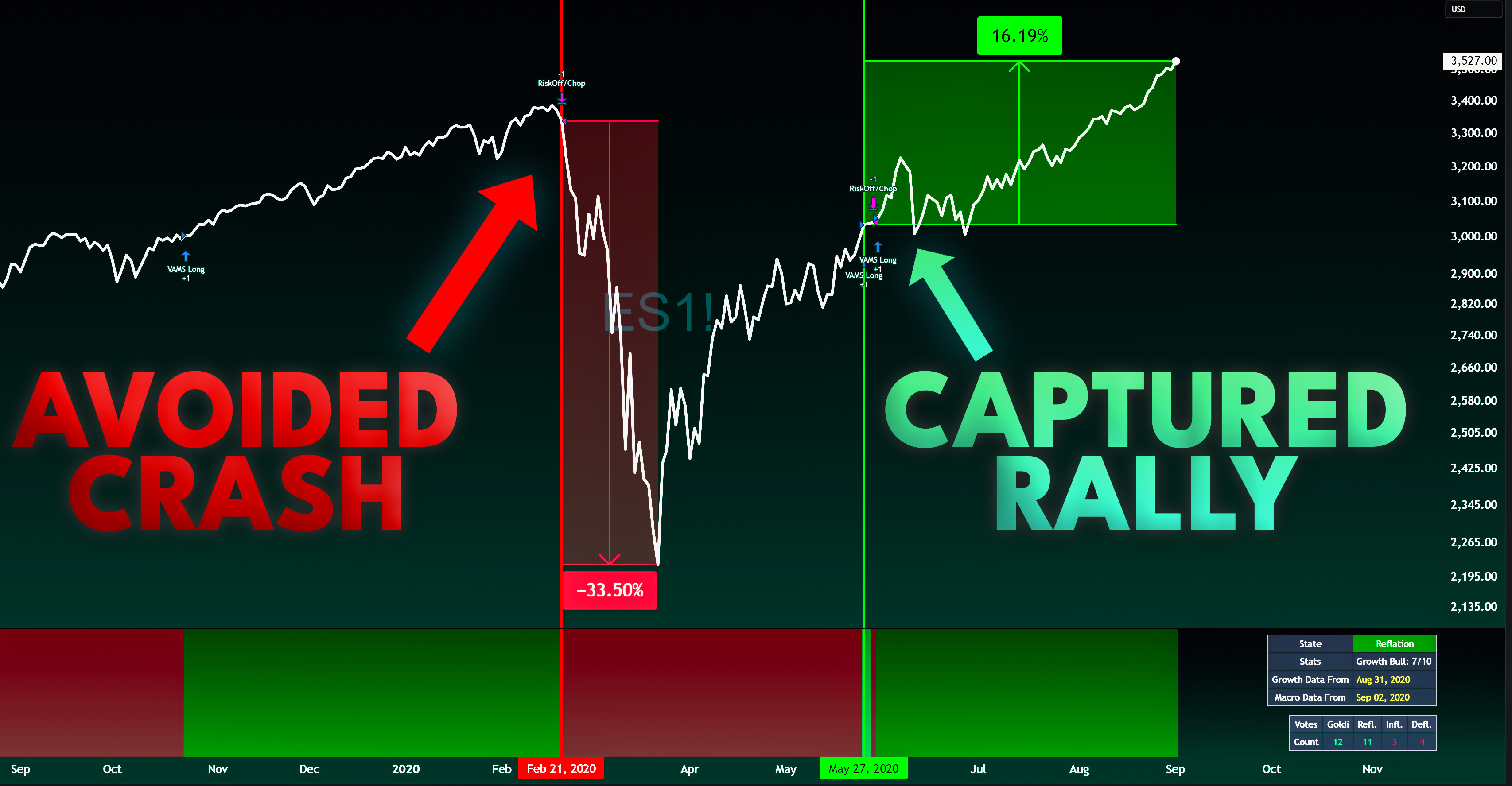

In February 2020, my Macro Regime Engine, a system that reads momentum signals across global equities, bonds, currencies, commodities, credit, and volatility to classify the macroeconomic environment.. exited its long position in the S&P 500.

The date was February 21st, 2020.

Over the following 23 trading days, the S&P 500 fell 34%.

The system didn’t predict COVID. It didn’t know a pandemic was coming. Nobody did.

What it did was something much simpler: it measured that the global macro environment had turned hostile.. across multiple independent asset classes, simultaneously, and it stepped aside.

This post walks through exactly what happened.

What Happened Next

The S&P 500 closed at 3,373 on February 19th.

By March 23rd, it hit 2,237. A 34% drawdown in 23 trading days.. the fastest bear market in history.

The system was in cash for the entire move.

The Recovery: Getting Back In

The system didn’t rush back in. Through March and April, while the market was bouncing violently off the lows, the macro breadth was still hostile. Growth assets were mixed. Volatility was elevated. Credit spreads were still wide. The vote count said: “this isn’t safe yet.”

By late May, that changed. Global equities had recovered enough breadth. Volatility was declining. Risk currencies were stabilizing. Credit spreads were tightening. The cross-asset picture shifted from “crisis” to “early recovery.”

The system re-entered on May 31, 2020. The S&P was at 3,054.

It held that position for 15 months.. through the entire reopening rally, through the vaccine rollout, through the melt-up into mid-2021. The trade returned +48.5% before the system exited again in September 2021, ahead of the 2022 bear market.

What This Tells You

The Macro Regime Engine didn’t time the top or the bottom. It entered the recovery about 36% above the absolute low. It exited the bull market a few weeks before the peak.

What it did was avoid the catastrophe in the middle.

A buy-and-hold investor who held through the COVID crash needed a 52% gain from the March bottom just to get back to the February high. And they had to endure the psychological reality of watching a third of their portfolio evaporate in three weeks.

The system was in cash, compounding from near the equity peak. When the recovery started, we had more capital to deploy. That advantage.. entering the next cycle from a higher base, is worth more than any individual trade.

This is the core thesis of the Macro Regime Engine: you don’t need to predict crises. You need to measure that the macro environment has turned hostile and step aside before the worst of the damage occurs. Cross-asset breadth gives you that measurement. No single chart can.

The Full Track Record

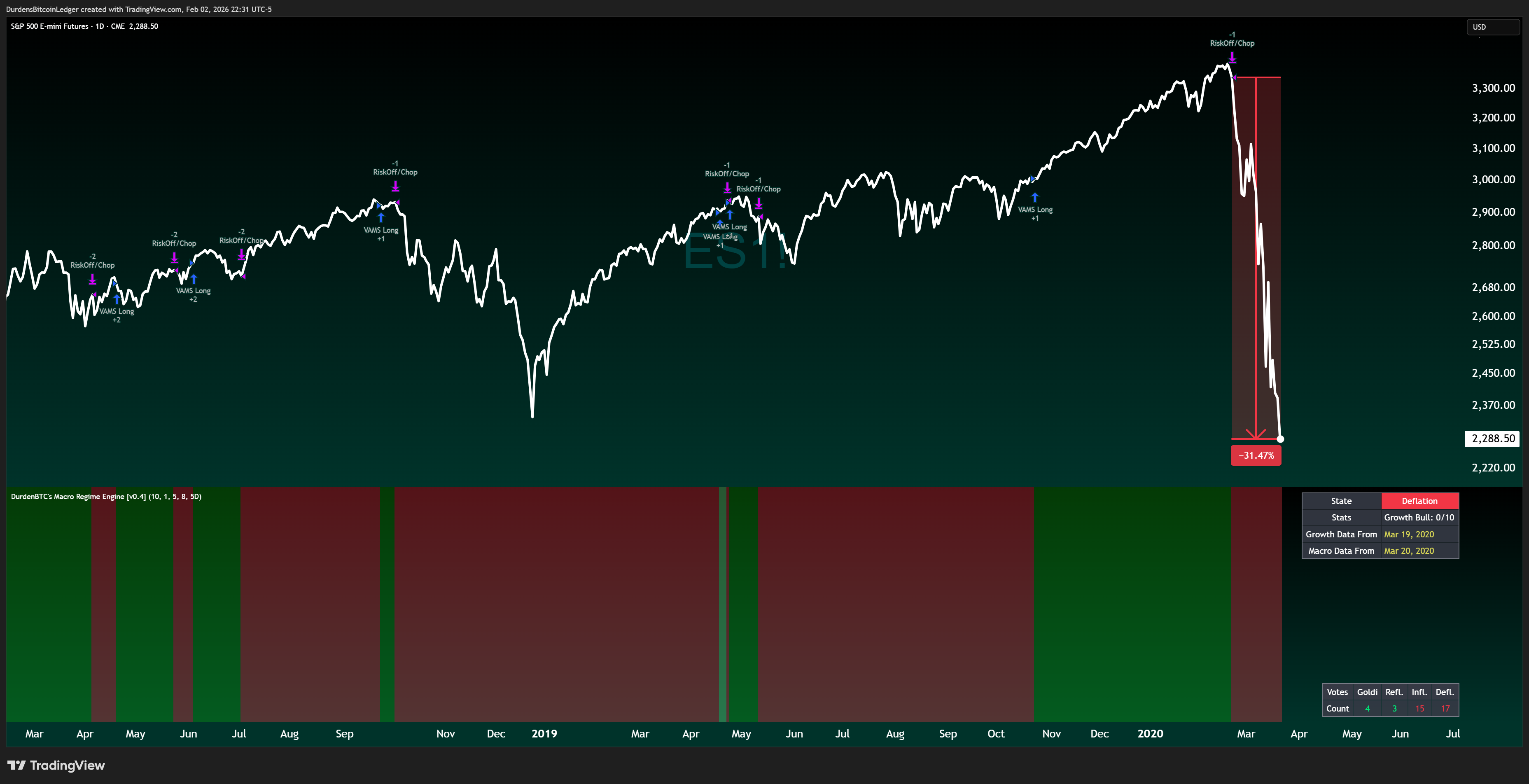

The COVID exit wasn’t a one-off. Over 26 years of backtesting on S&P 500 futures:

The system exited before the dot-com crash (September 2000)

It exited before the GFC waterfall (December 2007)

It exited the week before COVID (February 2020)

It exited near the top before the 2022 bear (November 2021)

75% win rate. 17:1 profit factor. 9.4% max drawdown across every major market crisis in modern history.

I share the regime signals with my subscribers. When the system flips, you’ll know what changed and why.

Disclaimer: This content is for educational and informational purposes only. It does not constitute financial advice. Past performance, whether backtested or live, does not guarantee future results.

Backtested results have inherent limitations and do not reflect actual trading. The author is not a licensed financial advisor. You are solely responsible for your own trading decisions.

Want the live dashboards behind these insights?

Subscribe on Substack Free subscribers get research updates. Paid subscribers get live macro tools + signal alerts.