TL;DR

Fed cut 25 bps, tone hawkish. Market priced it, liquidity backdrop still improves.

Data mixed but resilient. Retail sales beat, claims cooled, Empire weak, Philly strong.

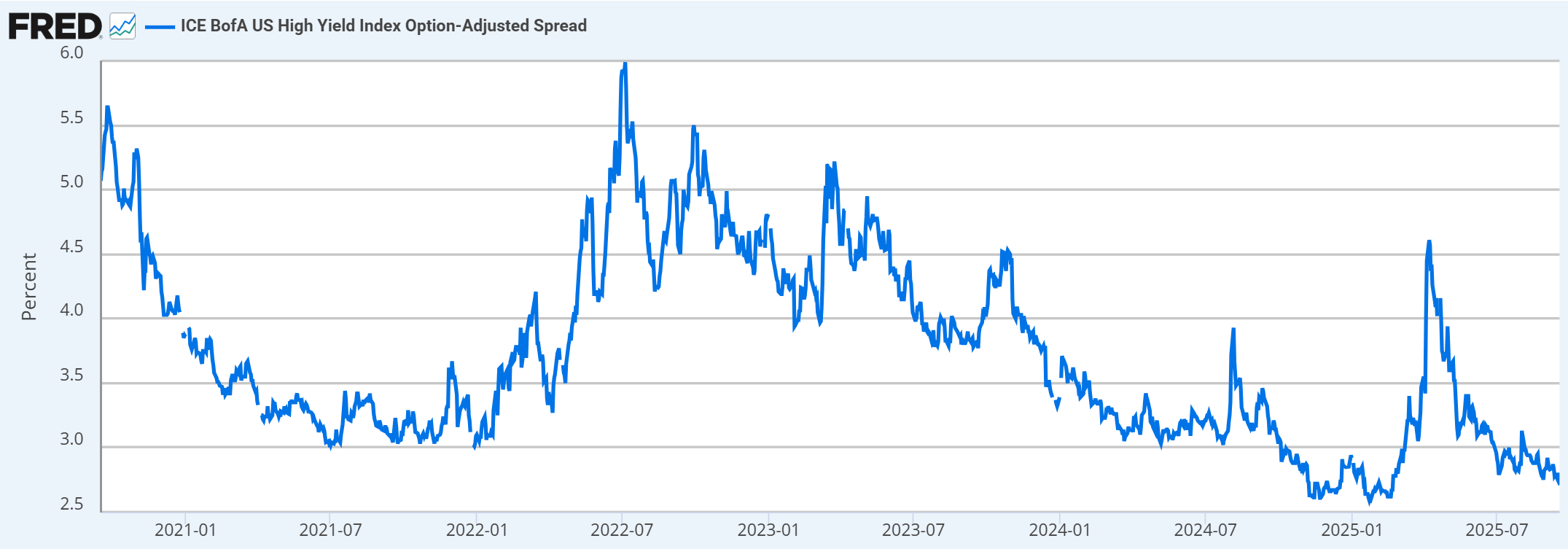

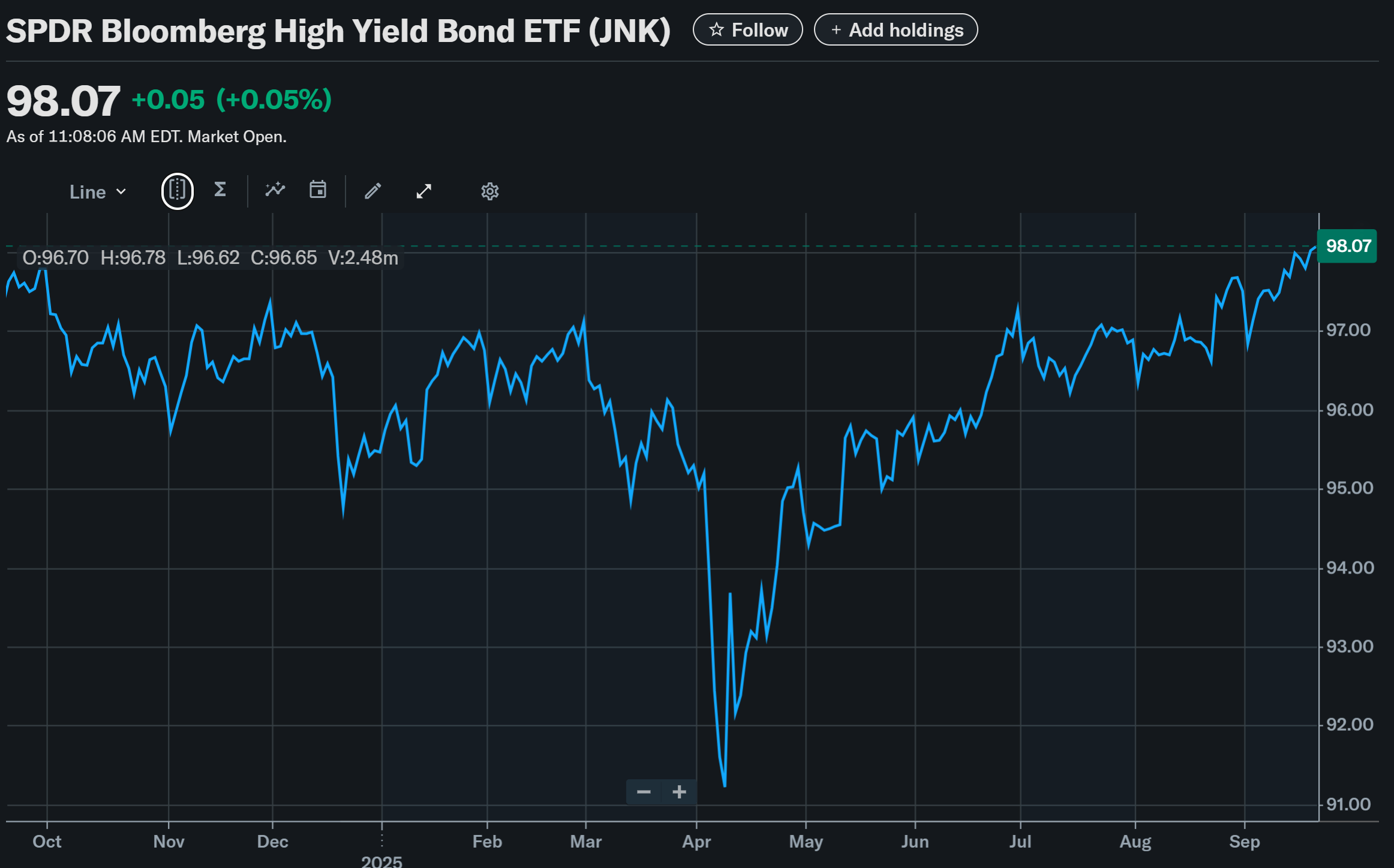

Credit says risk-on. High yield spreads low, HYG breaking out.

Global liquidity tilts positive. BoE slows QT, PBOC injects.

BTC≃NDX. Correlation is tight. Santa rally = ATH risk. NDX rollover = BTC downside.

The tape I care about:

Bitcoin’s September strength is an anomaly, but month isn’t over. The Macro Regime Tracker dipped to its lower rail, long-term signal still constructive. Keep powder dry, don’t over-position into month-end.

Liquidity and credit

BoE: Rate hold, QT slowed and skewed away from long gilts. Marginally supportive for global liquidity.

PBOC: ¥487B 7-day reverse repo injection, policy rate unchanged. Liquidity via OMOs, not rate cuts.

Credit risk tone: HY OAS is low, HYG broke out of a year-long base. Credit is confirming equities. That is typically bullish beta, including BTC.

On-chain and dollar lens

DXY trend filter: Still bullish for risk. Dollar easing tailwind remains.

STH realized price: Bounce held into early September, structure supportive.

MVC / cycle gauges: MVC not crossed 365-DMA yet, so the “full-send” signal isn’t on.

What flips me

NDX trend break with dollar strength and widening HY spreads.

PMIs roll hard and claims trend higher, not one-off noise.

Liquidity pullback from BoE/PBOC, or US issuance that soaks reserves.

If this helped, share it and subscribe so you get the War Room before the next print hits. Comments open — what are you watching into PMIs and quarter-end?

For the full video breakdown:

💥 Stay sharp. Stay sovereign. Don’t be exit liquidity.

— Durden out.

✊🧼

Not financial advice. Manage risk. The market’s real engine is liquidity.

Want the live dashboards behind these insights?

Subscribe on Substack Free subscribers get research updates. Paid subscribers get live macro tools + signal alerts.